Stamp Duty Relief & e-Invoicing Updates

The Inland Revenue Board of Malaysia (IRBM/LHDN) has published multiple significant updates in relation to stamp duty and implementation of e-Invoicing.

Stamp Duty Relief for Employment Contracts

The Ministry of Finance has granted a relief from stamp duty payments for any employment entered prior to 1 January 2025. The announcement is silent on other instruments such as service agreements including intragroup service agreements. Taxpayers should review the position with regards to such agreements considering the higher scrutiny by the IRBM on stamp duty matters in recent times.

For employment agreements entered into during the calendar year 2025, a grace period is granted until 31 December 2025 for stamping purposes. Given that multiple documentation may exist in relation to an employment (e.g. annual increment letters), businesses should carefully assess the impact of each of these documents pursuant to Stamp Act 1949.

A comprehensive compliance review – not confined to only employment agreements – is advisable given the legislative changes to implement Self-Assessment for Stamp Duty effective from 1 January 2026.

Limitation on Permissibility of Consolidated e-Invoice

Consolidated e-Invoice is a simpler mechanism compared to a transaction-specific e-Invoice as Buyer’s data does not have to be collected and reported to IRBM for the purposes of consolidated e-Invoice.

On 5 June 2025, a new restriction has been introduced whereby consolidated e-Invoice is not permitted for any transaction with value exceeding RM10,000. This restriction takes effect from 1 January 2026.

For transactions up to 31 December 2025, consolidated e-Invoice is permitted even for transactions with value exceeding RM10,000 (except for specified transactions for transaction-specific e-Invoice is mandatory – this includes sale of motor vehicles, flight tickets, private charter (in relation to aviation), construction and construction materials).

e-Invoicing Deferral & Exemption

The annual revenue threshold blanket exemption for micro and small businesses is increased from RM150,000 to RM500,000. This exemption applies to both incorporated businesses and unincorporated businesses. With this regard, businesses making payments to individuals should be diligent in determining whether or not the payee is carrying on the business. Should the payee be an individual who is not carrying on a business, the payer is obliged to issue a Self-Billed e-Invoice (SBeI) on such payment regardless of his/her annual income level.

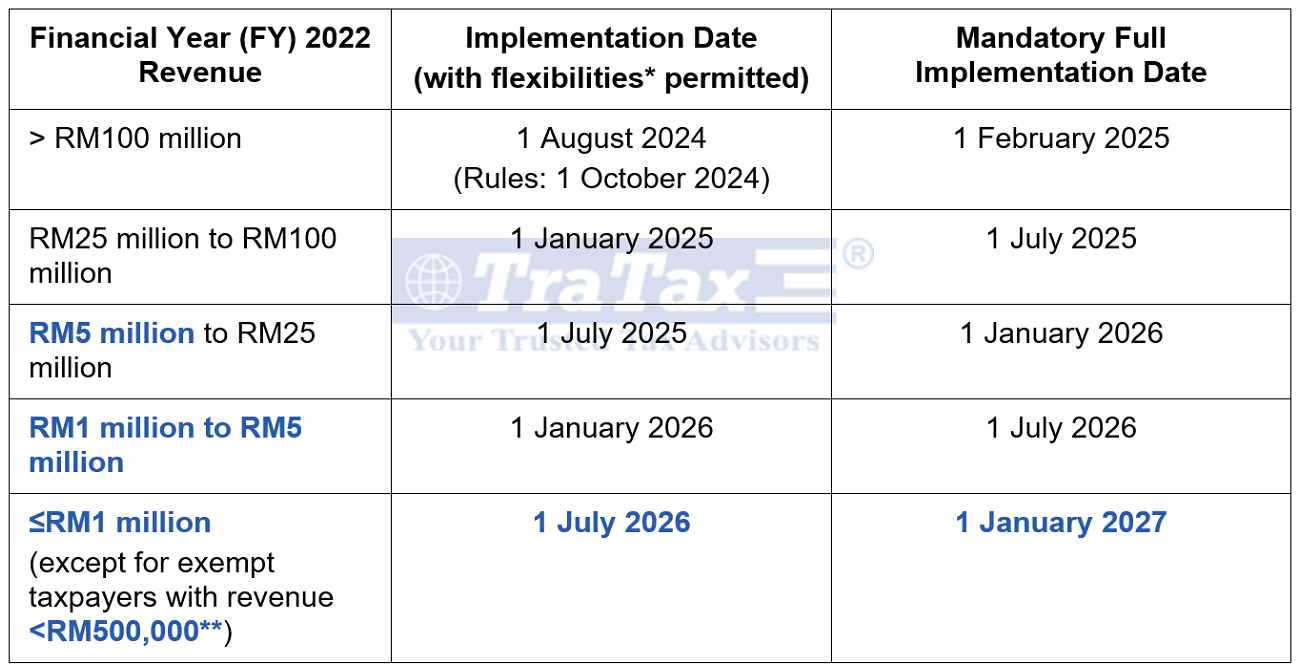

Further, the implementation timeline for businesses with annual revenue not exceeding RM5 million is deferred by 6 months. Below is a summary of the new e-Invoicing implementation timeline:

* During the initial 6-month period, greater flexibility is granted through the broader permissibility of consolidated e-invoice. The 6-month period is not immune from non-compliance penalty if the taxpayer fail to issue consolidated e-Invoice and consolidated self-billed e-Invoice for each month.

** While the implementation timeline is based on FY 2022 Revenue, the RM500,000 threshold for the purpose of blanket exemption is tested on annual basis. Should an exempt taxpayer reach the RM500,000 threshold at any time (say, Year 1), such person shall comply with e-Invoicing requirements from the beginning of Year 3. Also, the exemption is unlikely to apply to a taxpayer who is part of a larger group of companies.

If a business or operation commences at a time after the year 2022, the e-Invoice implementation date is 1 July 2026 or, if later, upon commencement of such business or operation (subject to the RM500,000 exemption).

Disclaimer: The information herein is simplified for brevity. Kindly seek case-specific consultation prior to any action. The write-up may contain our interpretation, to which the authorities and Courts may not necessarily concur. Strictly no liability assumed.